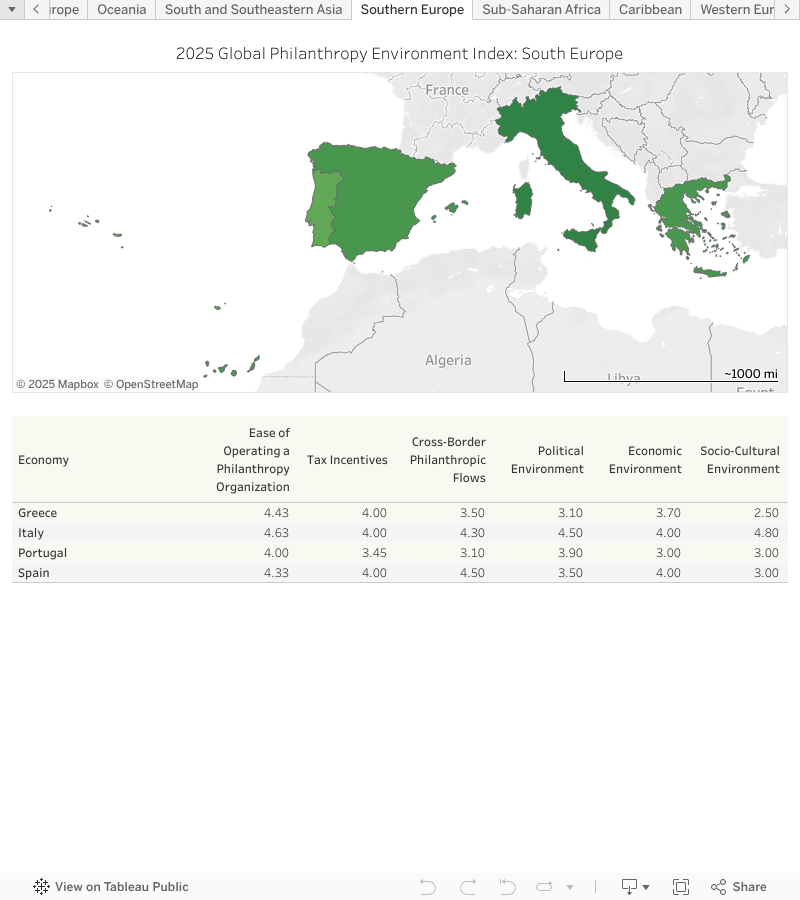

Southern Europe

Regional Reviewer: Marta Rey-García

Institutional Affiliation: University of A Coruña (UDC), Spain

Overview

Overall, the environment for philanthropy in Southern Europe has remained relatively stable between 2021 and 2023, particularly compared to the disruption caused by the COVID-19 crisis in 2020. Stability, though, should be interpreted as a balance of positive and negative developments, particularly in regard to the political and sociocultural environment for philanthropy.

Changes in the legal and tax environment for philanthropic organizations have been limited, incremental, and mostly related to the implementation of previously existing frameworks. The aftermath of the pandemic shock has anchored philanthropy in the context of broader recovery efforts and organizational support systems led by governments. This new environment has turned cross-sector and intra-sector collaboration (e.g., between philanthropic foundations and NGOs) into a mainstream practice with the potential to enhance the positive impacts of philanthropic organizations on both people and the planet.

Global trends already affecting the region before 2020 accelerated their pace between 2021 and 2023. The speed of digital transformation of philanthropic organizations and their relations with relevant stakeholders, including employees and donors, increased in the aftermath of COVID-19, parallel to the augmented visibility and urgency of natural disasters and other challenges derived from climate change. Overall, the economy got back on track thanks to recovery and resilience plans and despite new circumstantial crises—for example, energy and inflation, compounded with external shocks; natural catastrophes; wars in Ukraine and Gaza; and structural challenges in the region, such as the arrival of refugees and migrants. The escalation of the war in Ukraine, due to Russia’s February 2022 invasion, imperiled food security and energy supply in the EU, disproportionately impacting the most vulnerable segments of the population and spreading Ukrainian refugees across Europe.

These crises, combined with changing social needs, elicited emergency responses on the part of philanthropic organizations. These acute responses have been blended with more long-range work on both traditional and emerging issues, from the elderly to the ethical use of Artificial Intelligence (AI). Toning down perceptions of regional stability and incremental improvements, however, is a concern among country experts about the negative effects on philanthropy and civil society, including increased political polarization and cultural distrust.

View the full 2025 GPEI Southern Europe regional report:

View the 2025 Country Reports for the Southern Europe region:

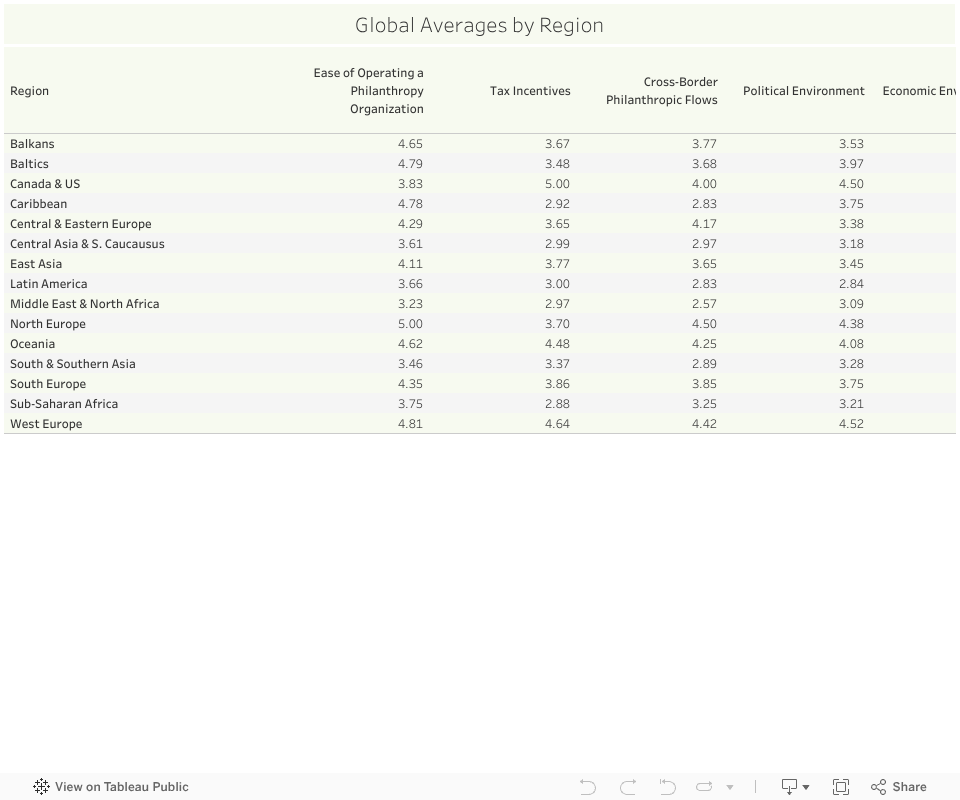

Regional Comparison: Global Philanthropy Environment Index (GPEI) Scores